【房产不快讯】卡城2018年8月-失业率延缓了房市的恢复

卡城老方房地产

不仅仅是房产,还会不定期提供有关卡城教育、生活等各方面实用信息

卡尔加里市,2018年9月4日讯:销售低迷、新上市量的增加以及库存量的增加让卡城8月的房地产市场回升乏力。

持续的过量供应让8月的房产价格继续下调。全市房屋基准价格比上月下降0.8%,比去年同期下降2.4%。

卡尔加里地产局首席经济师这样说:“卡尔加里失业率一直居高不下,现在已达到7.9%,还丢失了不少全职工作。就业市场的不景气是影响房产市场的重要因素之一。另外石油行业的缓慢恢复加上贷款条件的收紧以及新建房屋的竞争也都在影响房产市场。“

8月卡尔加里全市总共售出1490套,比去年同期下降近7%,比长期平均低14%。但并不是所有区域和类型的房产销售数量和价格都在下降。与去年相比,最近大多数区域的房产价格有所下降,而市中心区和西区与去年同期水平相当。

卡尔加里地产局主席这样说:”不论买家还是卖家都需要现实对待其期望值。买家需要明白价格变化并不是一概而论的,而是取决于他要买房屋的位置和特点。销量的下降并不就意味着价格也下降。卖家需要及时全面地了解市场行情,让他的卖价更有竞争力。卖家需要了解周边房产的销售情况以及对比已经卖出的房屋。“

8月卡城房产概况:

独立屋:

年初至今,几乎每个区域的独立屋销售都在放缓。增加的库存使房屋销售月数快达到5了,并且会继续影响房屋的价格;

8月独立屋的基准价格为49.7万。比上月低了0.74%,比去年同期低了2.6%。

8月大多数区域的房屋价格保持下行趋势,但西区和中心区仍比去年同期要高。

年初至今的平均ji准价格比去年低了0.56%,抵消了从去年开始的部分价格增长。

公寓

年初至今共售出1892套公寓,比去年同期降低了7%。但并不是所有区域销量都下滑。东北区和西北区的公寓销售略高于去年水平。Y

新上市量与去年相比有所放缓,防止了库存水兵的大幅增长。然而公寓仍是供过于求,导致价格继续下行。

年初至今全市公寓价格降了近3%,其中价格下滑最大的是东北区、南区和东区。整体价格比2014年的高点低了14%。

联排和双拼

和公寓一样,联排和双拼的销量也有所下降。但年初至今,一些区域销量有所改善,比如西北和西区的双拼屋。

东北区和东区的联排销售相对稳定。

双拼屋的供过于求今年已经对价格产生了下行压力,但中心区、东北区和东区的年初至今平均基准价格要高于去年。抵消了其他区域价格的下滑,是整个双拼屋的价格比去年高1%。

年初至今联排的价格比去年低了1.5%。但各区价格变动不一,市中心和西北区相对稳定,东北区跌了近7%。

常用房地产统计术语:

销售与上市比率(the sales-to-new listings ratio):给定期间的当前销售套数对比新上市套数,一般采用过去30天的数据。此比率一般是一个百分数,如果在40-60%之间,代表市场比较平衡,如果高于60%,一般指卖方市场,如果低于40%,一般代表买方市场。

房屋库存月数(Months of Supply):给定时间段(通常是过去30天)结束时库存总数除以同一时期结束时的销售总数。库存月数是房屋供求平衡的另一重要指标。它代表以目前的销售活动完全清算当前库存需要多长时间。

Media release: Unemployment rate slows housing market recovery

City of Calgary, September 4, 2018 – Easing sales, gains in new listings and elevated inventory levels continue to slow Calgary’s recovery in the housing market in August.

Persistent oversupply in the Calgary housing market continued to weigh on prices in August. Citywide benchmark prices edged down over previous months by 0.8 per cent and are 2.4 per cent below last year’s levels.

“Calgary’s employment market has persistently high unemployment rates at 7.9 per cent and recent job losses in full time positions. The struggles in the employment market are one of the factors weighing on our local housing market,” said CREB® chief economist Ann-Marie Lurie.

“A slow recovery in the energy sector combined with tighter lending conditions and competition from the new home sector are also contributing current housing market conditions.”

Citywide sales totaled 1,490 units this month, down nearly seven per cent from last year and 14 per cent below long-term trends.

Sales and price declines were not consistent across all districts and product types. Prices have recently trended down across most areas based on year-to-date figures, but have remained comparable to last year’s levels in the City Centre and West districts of the city.

“Both buyers and sellers need to be realistic about their objectives. Buyers need to be aware that price changes differ depending on what and where you are buying. The decline in sales does not mean price declines across the board,” said CREB® president Tom Westcott.

“Sellers need to be well informed to be competitive. They need a good understanding of what has been selling around them and how their property compares to homes that have successfully sold.”

HOUSING MARKET FACTS

Detached

Year-to-date detached sales eased across each district. Elevated inventory levels caused months of supply to remain just below five months in August and continued to weigh on housing prices across all districts.

Detached benchmark prices totaled $497,000 in August. This is a 0.74 per cent decline over last month and 2.6 per cent below the previous year.

Prices have trended down in all districts in August, however, on a year-to-date basis prices remain above last year in both the City Centre and West.

Year-to-date average detached benchmark prices have eased by 0.56 per cent over the previous year, reducing some of the price recovery from last year.

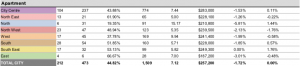

Apartment

Year-to-date sales totaled 1,892 units, seven per cent below the previous year. However, sales did not ease across all districts. Sales in both the North East and North West districts remained slightly higher than levels recorded last year.

New listings in the apartment sector eased compared to the previous year, preventing more significant gains in inventory levels. However, oversupply in this sector persists, causing further price declines.

Year-to-date city-wide prices eased by nearly three per cent, with the largest declines occurring in the North East, South and East districts. Overall prices remain nearly 14 per cent below 2014 highs.

Attached

Like the apartment sector, sales have eased in the attached sector. However, year-to-date sales have improved in some districts of the city for semi-detached and row product. Semi-detached sales improved in both the North West and West districts.

Row sales remained relatively stable in both the North East and East districts of the city.

Oversupply in the semi-detached sector has placed some downward pressure on prices this year, but year-to-date average benchmark price remains higher than last year in the City Centre, North

East and East districts of the city. Gains in these areas were enough to offset declines in other areas, keeping semi-detached prices one per cent higher than last year.

Year-to-date row prices eased by 1.5 per cent over last year. However, price movements ranged from relatively stable levels in the City Centre and North West to declines of nearly seven per cent in the North East district.

REGIONAL MARKET FACTS

Airdrie

Sales activity in Airdrie continued to ease compared to last year totalling 851 units so far this year.

Despite some of the recent pullback in new listings, year-to-date new listings remain just above last years levels keeping inventories elevated at 597 units.

The persistent oversupply in the market started to weigh on homes prices. Detached home prices totaled $366,900, 0.7 per cent below last month and 3.4 per cent below last year. When considering year-to-date averages, the benchmark price is 1.5 per cent below last years levels.

Cochrane

Year-to-date sales activity in Cochrane totaled 431 units. This is a decline over the previous year, but activity remains comparable to activity recorded over the past five years. This makes it a centre that has not seen the same pullback in demand seen in many other areas.

The challenge in the Cochrane area is the continued rise in supply. New listings continue to rise and are well above normal levels for the area. This has pushed up inventories to new highs, causing the months of supply to rise.

The excess supply in the area is starting to weigh on prices. Detached benchmark home prices in August edged down over the previous month to $426,100. Despite the recent easing, prices remain comparable to the previous year both for the month of August and year-to-date average figures.

Okotoks

Easing sales in Okotoks were met with further gains in new listings causing inventory levels to edge up to 280 units.

Recent gain in inventory compared to sales have placed some downward pressure on prices in the area. However, the easing was not enough to cause year-to-date prices to fall below last years levels.

Detached benchmark prices averaged $436,350 so far this year, just above last year’s levels.

常用房地产统计术语:

销售与上市比率(the sales-to-new listings ratio):给定期间的当前销售套数对比新上市套数,一般采用过去30天的数据。此比率一般是一个百分数,如果在40-60%之间,代表市场比较平衡,如果高于60%,一般指卖方市场,如果低于40%,一般代表买方市场。

房屋库存月数(Months of Supply):给定时间段(通常是过去30天)结束时库存总数除以同一时期结束时的销售总数。库存月数是房屋供求平衡的另一重要指标。它代表以目前的销售活动完全清算当前库存需要多长时间。

如果觉得文章有帮助,把它分享出去,帮助更多的人,

请扫描下边的二维码,加我微信:

也请点击或者扫描下边的二维码,关注我的公众号:)

有关房地产或者卡尔加里生活方面的问题,可以打电话或者加我微信,知无不言,言无不尽:)

点击原文,可以转到我的网站,上边有更多的资讯,欢迎光临。

卡城老方房地产

不仅仅是房产,还会不定期提供有关卡城教育、生活等各方面实用信息

卡尔加里市,2018年9月4日讯:销售低迷、新上市量的增加以及库存量的增加让卡城8月的房地产市场回升乏力。

持续的过量供应让8月的房产价格继续下调。全市房屋基准价格比上月下降0.8%,比去年同期下降2.4%。

卡尔加里地产局首席经济师这样说:“卡尔加里失业率一直居高不下,现在已达到7.9%,还丢失了不少全职工作。就业市场的不景气是影响房产市场的重要因素之一。另外石油行业的缓慢恢复加上贷款条件的收紧以及新建房屋的竞争也都在影响房产市场。“

8月卡尔加里全市总共售出1490套,比去年同期下降近7%,比长期平均低14%。但并不是所有区域和类型的房产销售数量和价格都在下降。与去年相比,最近大多数区域的房产价格有所下降,而市中心区和西区与去年同期水平相当。

卡尔加里地产局主席这样说:”不论买家还是卖家都需要现实对待其期望值。买家需要明白价格变化并不是一概而论的,而是取决于他要买房屋的位置和特点。销量的下降并不就意味着价格也下降。卖家需要及时全面地了解市场行情,让他的卖价更有竞争力。卖家需要了解周边房产的销售情况以及对比已经卖出的房屋。“

8月卡城房产概况:

独立屋:

年初至今,几乎每个区域的独立屋销售都在放缓。增加的库存使房屋销售月数快达到5了,并且会继续影响房屋的价格;

8月独立屋的基准价格为49.7万。比上月低了0.74%,比去年同期低了2.6%。

8月大多数区域的房屋价格保持下行趋势,但西区和中心区仍比去年同期要高。

年初至今的平均ji准价格比去年低了0.56%,抵消了从去年开始的部分价格增长。

公寓

年初至今共售出1892套公寓,比去年同期降低了7%。但并不是所有区域销量都下滑。东北区和西北区的公寓销售略高于去年水平。Y

新上市量与去年相比有所放缓,防止了库存水兵的大幅增长。然而公寓仍是供过于求,导致价格继续下行。

年初至今全市公寓价格降了近3%,其中价格下滑最大的是东北区、南区和东区。整体价格比2014年的高点低了14%。

联排和双拼

和公寓一样,联排和双拼的销量也有所下降。但年初至今,一些区域销量有所改善,比如西北和西区的双拼屋。

东北区和东区的联排销售相对稳定。

双拼屋的供过于求今年已经对价格产生了下行压力,但中心区、东北区和东区的年初至今平均基准价格要高于去年。抵消了其他区域价格的下滑,是整个双拼屋的价格比去年高1%。

年初至今联排的价格比去年低了1.5%。但各区价格变动不一,市中心和西北区相对稳定,东北区跌了近7%。

常用房地产统计术语:

销售与上市比率(the sales-to-new listings ratio):给定期间的当前销售套数对比新上市套数,一般采用过去30天的数据。此比率一般是一个百分数,如果在40-60%之间,代表市场比较平衡,如果高于60%,一般指卖方市场,如果低于40%,一般代表买方市场。

房屋库存月数(Months of Supply):给定时间段(通常是过去30天)结束时库存总数除以同一时期结束时的销售总数。库存月数是房屋供求平衡的另一重要指标。它代表以目前的销售活动完全清算当前库存需要多长时间。

Media release: Unemployment rate slows housing market recovery

City of Calgary, September 4, 2018 – Easing sales, gains in new listings and elevated inventory levels continue to slow Calgary’s recovery in the housing market in August.

Persistent oversupply in the Calgary housing market continued to weigh on prices in August. Citywide benchmark prices edged down over previous months by 0.8 per cent and are 2.4 per cent below last year’s levels.

“Calgary’s employment market has persistently high unemployment rates at 7.9 per cent and recent job losses in full time positions. The struggles in the employment market are one of the factors weighing on our local housing market,” said CREB® chief economist Ann-Marie Lurie.

“A slow recovery in the energy sector combined with tighter lending conditions and competition from the new home sector are also contributing current housing market conditions.”

Citywide sales totaled 1,490 units this month, down nearly seven per cent from last year and 14 per cent below long-term trends.

Sales and price declines were not consistent across all districts and product types. Prices have recently trended down across most areas based on year-to-date figures, but have remained comparable to last year’s levels in the City Centre and West districts of the city.

“Both buyers and sellers need to be realistic about their objectives. Buyers need to be aware that price changes differ depending on what and where you are buying. The decline in sales does not mean price declines across the board,” said CREB® president Tom Westcott.

“Sellers need to be well informed to be competitive. They need a good understanding of what has been selling around them and how their property compares to homes that have successfully sold.”

HOUSING MARKET FACTS

Detached

Year-to-date detached sales eased across each district. Elevated inventory levels caused months of supply to remain just below five months in August and continued to weigh on housing prices across all districts.

Detached benchmark prices totaled $497,000 in August. This is a 0.74 per cent decline over last month and 2.6 per cent below the previous year.

Prices have trended down in all districts in August, however, on a year-to-date basis prices remain above last year in both the City Centre and West.

Year-to-date average detached benchmark prices have eased by 0.56 per cent over the previous year, reducing some of the price recovery from last year.

Apartment

Year-to-date sales totaled 1,892 units, seven per cent below the previous year. However, sales did not ease across all districts. Sales in both the North East and North West districts remained slightly higher than levels recorded last year.

New listings in the apartment sector eased compared to the previous year, preventing more significant gains in inventory levels. However, oversupply in this sector persists, causing further price declines.

Year-to-date city-wide prices eased by nearly three per cent, with the largest declines occurring in the North East, South and East districts. Overall prices remain nearly 14 per cent below 2014 highs.

Attached

Like the apartment sector, sales have eased in the attached sector. However, year-to-date sales have improved in some districts of the city for semi-detached and row product. Semi-detached sales improved in both the North West and West districts.

Row sales remained relatively stable in both the North East and East districts of the city.

Oversupply in the semi-detached sector has placed some downward pressure on prices this year, but year-to-date average benchmark price remains higher than last year in the City Centre, North

East and East districts of the city. Gains in these areas were enough to offset declines in other areas, keeping semi-detached prices one per cent higher than last year.

Year-to-date row prices eased by 1.5 per cent over last year. However, price movements ranged from relatively stable levels in the City Centre and North West to declines of nearly seven per cent in the North East district.

REGIONAL MARKET FACTS

Airdrie

Sales activity in Airdrie continued to ease compared to last year totalling 851 units so far this year.

Despite some of the recent pullback in new listings, year-to-date new listings remain just above last years levels keeping inventories elevated at 597 units.

The persistent oversupply in the market started to weigh on homes prices. Detached home prices totaled $366,900, 0.7 per cent below last month and 3.4 per cent below last year. When considering year-to-date averages, the benchmark price is 1.5 per cent below last years levels.

Cochrane

Year-to-date sales activity in Cochrane totaled 431 units. This is a decline over the previous year, but activity remains comparable to activity recorded over the past five years. This makes it a centre that has not seen the same pullback in demand seen in many other areas.

The challenge in the Cochrane area is the continued rise in supply. New listings continue to rise and are well above normal levels for the area. This has pushed up inventories to new highs, causing the months of supply to rise.

The excess supply in the area is starting to weigh on prices. Detached benchmark home prices in August edged down over the previous month to $426,100. Despite the recent easing, prices remain comparable to the previous year both for the month of August and year-to-date average figures.

Okotoks

Easing sales in Okotoks were met with further gains in new listings causing inventory levels to edge up to 280 units.

Recent gain in inventory compared to sales have placed some downward pressure on prices in the area. However, the easing was not enough to cause year-to-date prices to fall below last years levels.

Detached benchmark prices averaged $436,350 so far this year, just above last year’s levels.

常用房地产统计术语:

销售与上市比率(the sales-to-new listings ratio):给定期间的当前销售套数对比新上市套数,一般采用过去30天的数据。此比率一般是一个百分数,如果在40-60%之间,代表市场比较平衡,如果高于60%,一般指卖方市场,如果低于40%,一般代表买方市场。

房屋库存月数(Months of Supply):给定时间段(通常是过去30天)结束时库存总数除以同一时期结束时的销售总数。库存月数是房屋供求平衡的另一重要指标。它代表以目前的销售活动完全清算当前库存需要多长时间。

如果觉得文章有帮助,把它分享出去,帮助更多的人,

请扫描下边的二维码,加我微信:

也请点击或者扫描下边的二维码,关注我的公众号:)

有关房地产或者卡尔加里生活方面的问题,可以打电话或者加我微信,知无不言,言无不尽:)

点击原文,可以转到我的网站,上边有更多的资讯,欢迎光临。